The internet is buzzing with shock and outrage at today’s announcement that Andreessen Horowitz (a16z) is investing $350 million in Flow, the new startup of the arguably disgraced co-founder of WeWork, Adam Neumann. Even before opening its doors or having a product, this funding round values Flow at more than $1 billion.

People seem skeptical at best, angry at worst about Adam raising this much money so soon after WeWork’s flop – its loss of value for shareholders and toxic employee culture of sexism. (I often find it challenging to succinctly summarize the misdeeds of people in positions of power who also happen to be white men, so if you have a better summary, feel free to leave a comment.)

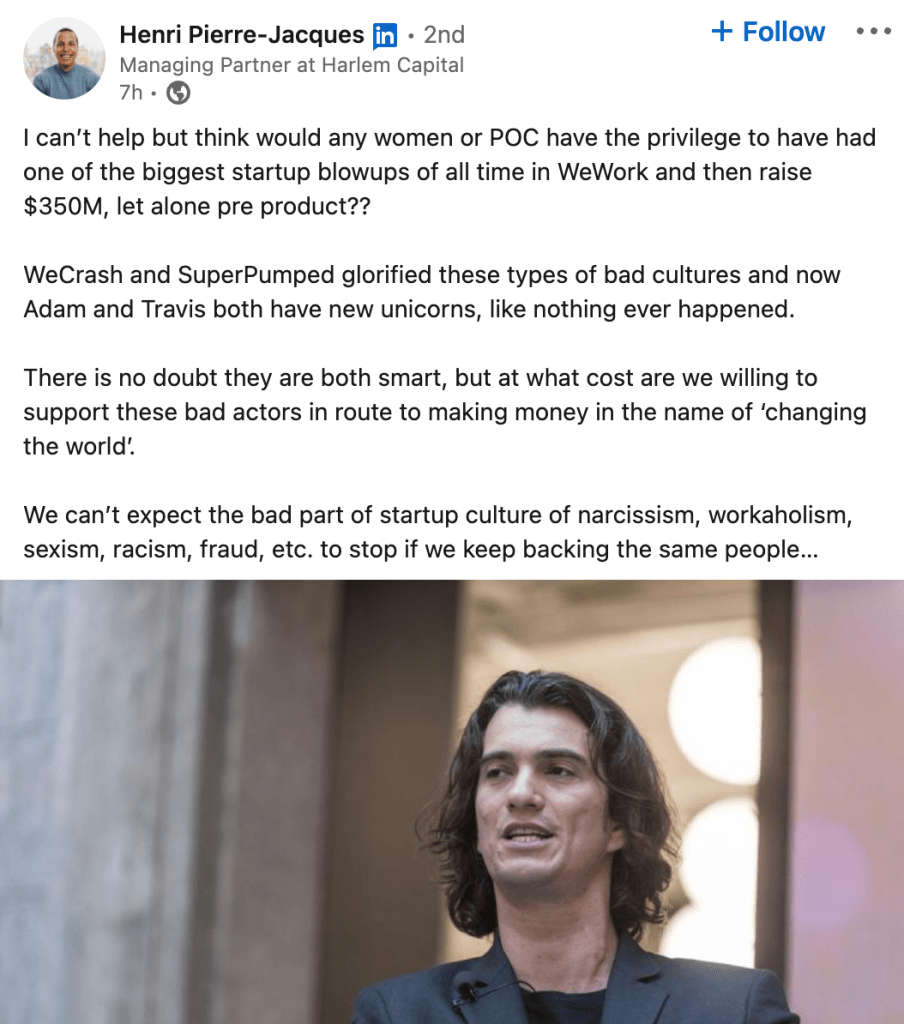

There are some nuanced takes like this Linkedin post from Henri Pierre-Jacques of Harlem Capital.

Building on Henri’s line of inquiry, let’s talk about what no one has really brought up yet…

How does a venture deal like this happen? Who makes this possible?

a16z’s Limited Partners

Who invests in a16z? What do the LPs think about this deal? Have reporters interviewed these LPs whose money is invested in Flow?

Let’s follow the money – and look at the money behind the money:

- a16z invested $350m in Flow, but a16z also has investors (Limited Partners) such as university endowments, pension plans, sovereign wealth funds, family offices, a16z partners / employees, and other individuals (including a selected group of Black LPs out of its Cultural Leadership Fund). These Limited Partners invest in a16z (General Partner) who invests in startups like Flow.

- a16z deals and funds may have generated so much money that they are reducing their dependence on outside capital, but they are still raising it

- a16z raises raised large funds for specific strategies ($4.5bn crypto; $2bn late stage; $750m for early-stage) which means – on average – they need to write large checks to deploy their capital.

What are some other facts according to New York Times’s Dealbook:

- “The investment, the largest individual check Andreessen Horowitz has ever written in a round of funding to a company”

- “Flow is expected to launch in 2023, and Marc Andreessen will join its board”

- “Neumann has purchased more than 3,000 apartment units in Miami, Fort Lauderdale, Atlanta and Nashville. His aim is to rethink the housing rental market by creating a branded product with consistent service and community features. Flow will operate the properties Neumann has bought and also offer its services to new developments and other third parties. Exact details of the business plan could not be learned.”

- “Flow appears to be financially separate from the crypto company Flowcarbon, which was also co-founded by Neumann and raised $70 million in May in a round led by Andreesen Horowitz.”

- “Andreessen said in the blog post that he was interested in Flow because the rental real estate market is ripe for disruption.”

Reading between the lines, a few observations and thoughts:

- This investment represents not only an inconsistency to average industry check size and in their firm’s history, especially for a deal at this stage. $350m is a large check (the largest in the firm’s history in 1 round) in general (and would make more sense for later-stage deals), but unheard of for a pre-seed deal (industry average check sizes at $500k-$1m at $X-$XXm valuations). So how why did this get 100-350x for this deal?

- Andreesen Horowitz must have really wanted this deal, wanted to work with Adam, wanted that board seat, wanted to lead this deal?

- Why would a16z make such a large bet again, after investing $70m in Neumann’s Flowcarbon company only 3 months ago?

- “Disruption” = $$$ opportunity – there’s clearly potential to create another multi-billion dollar business, but how? With what business model?

Returns, but at what cost?

What if – in the process of “rethinking the rental market” and “disrupting residential real estate,” Flow employs an exploitive business model that ends up gentrifying low income Americans in BIPOC neighborhoods and communities? Squeezing the pocketbooks and ultimately bankrupting… let’s say, public school teachers? Ends up making structural changes to the residential real estate market that harms middle class Americans and exacerbates existing inequities that can’t easily be reversed?

Hm, so if I’m a pension fund, do I tell my employees, “well, your pension holdings are up 3% due to an exit in Flow, but that same company contributed to your eviction or is related to why it’s been harder to find an affordable home of your choice (that isn’t full of amenities that you actually don’t want) or ”

If I were an LP in a16z’s fund, I would be paying close attention to not only my financial returns, but impact of my portfolio and its potential inadvertent harms on the very people whose futures I’m trying to protect and nurture.

What could LP accountability look like?

LPs might not be in a position to take immediate, direct action, but can start to think about the second and third order effects of their investments in fund managers — as well as potential sources or causes of these dynamics, such as fund sizes.

- Fund sizes – what incentives do mega funds create? do larger funds create incentives for undisciplined behavior?

- Inadvertent harms – what harms, if any, have the companies caused my stakeholders or in the world?

Fund Size in Focus:

Larger funds tend to lead to larger investments in companies who then are in turn saddled with aggressive growth or expansion goals to generate a return on a larger amount of capital. Disproportionately large funds create an environment ripe for bad incentives – with startups looking to find hacks, loopholes, shortcuts, or even commit fraud – to deliver. Companies also may attempt to fundraise more to make up for their losses or burn rates, resulting in unsustainable business models that put pressure on the need for a large exit.

Why is this hard?

Everyone’s incentives are askew. Everyone is incentivized to maintain the status quo, especially the status quo has been making them money.

- Cash money – Venture capital funds get richer as they raise larger and larger funds. ^^ This is oversimplified – but worth saying. Firms typically charge a 2% management fee annually for the first 5 years of the fund – so the larger the fund ($100M fund VS $500M fund VS $1B fund), so you are pocketing $2M, $10M, or $20M every year.

- Symbiotic relationships – Employees, startup founders, and others in the ecosystem don’t want to “bite the hand that feeds them.” The people who have information also do benefit from the system writ large – whether it’s through their paychecks, investment track records, industry signaling / credibility, references, or getting to the next valuation round to support their companies. At that point, you want the deals to do well and to make money together. And these are people that you might be friends with, went to college or b-school with, and generally like. They can be speak persuasively, be charismatic, and even make you feel seen and heard.

- Fear of retaliation – VCs like a16z and others have a history of not only criticizing but also targeting journalists through various tactics of online harassment.

- Power imbalances – when times are good and fund performance is up, GPs / VCs have the power. Demand to invest in their funds is high, so GPs can pick and choose which LPs to let in. The best performing funds can be “hard to access” and get into, so LPs may feel less comfortable requesting custom or extra analysis or information, especially if the GP is generating great returns for them.

A few thoughts on “disruption”

I think after the general public bought into the Silicon Valley hype and startup/tech manta popularized by Facebook of “move fast and break things,” the public has growing awareness of that not all disruption is good. People are starting to wonder, “disruption, but at what cost?” While I recognize there are companies that have transformed how we live and work, but so many companies today are setting out to “disrupt this” and “democratize that.”

How can people trust that Flow isn’t another form of greenwashing – with purpose masquerading as content marketing for profit?

Perhaps only time will tell, but it’s been interesting to see people’s reactions. I am hopeful that with the increase in public consciousness of incentives and bad actors in the last 5+ years, we don’t forget the lessons of the past and think critically before blindly consuming or supporting purpose-driven corporations… because at the end of the day, that’s what they are: corporations.

Leave a comment